Earn: How to Make The Most of Your Income Today and Save Enough for Tomorrow

Posted by Rebecca Harbrow on Friday 5th January 2024.

How to make the most of your income today and save enough for tomorrow

Create your budget in four steps

Create your budget in four steps

Setting up a budget won’t take long, and if you stick to it then you could boost your savings at the same time. Your budget should chart your income, outgoings and financial goals and give you a spending plan to follow.

A budget can put you in control of your money because you’ll know exactly where each pound is being spent (or saved). And any savings you make in a month or money you bring in in addition to your regular income can be included in your budget.

Most importantly a budget can help you save and plan for the fun stuff in your life, whether it’s a holiday or something on your wish list.

Here’s how to get started:

1. What’s your income?

Record your earnings every month – this means your income after tax and deductions, and any other income (like freelance work or rental income). Try to save around 10% of your net income each month.

2. List your monthly fixed costs

For example, rent or mortgage, utility bills, council tax, memberships or subscriptions, groceries, childcare and transport. Also include debts and loans like credit card balances, loan payments and overdrafts.

3. Minus your fixed costs from your monthly income

Your result should leave you with some money spare. If not, what adjustments could you make to help you get there? Are there subscriptions or items you could cut to help you save?

4. What are you aiming for?

Do you have an overall goal – like saving for a new car or paying off a loan or credit card? See how much you can set aside once you’ve done your calculation.

Don’t forget your emergency fund

Budgeting can help you build an emergency fund – which is an amount of cash set aside to cover around two to three months of essentials in case something unexpected happens. By having a plan for your money and staying in control of it, you’ll be in a stronger position to handle sudden and unexpected expenses.

It pays to pay into your pension

If your workplace has a pension scheme for its employees, part of your wage will automatically be paid into it every month. You might be tempted to reduce your contribution or even cancel it if you’re decades away from retirement or could do with a little more in your pay packet each month.

However, statistics show that many of us do not have enough in our pension pot for our retirement when the time comes. Most employees say their pension will only provide enough money to “just get by” in retirement (39%). Making regular contributions throughout your working life is important to make sure you can enjoy a comfortable retirement.

Many employers match your voluntary contributions up to a certain limit, so you would not only be losing out on your own contributions but potentially on the value your employer would match. If you start paying into your pension earlier, the more tax relief you’ll receive and the more time your overall pot will potentially have to grow.

How much are you putting into savings?

Here’s a common 50/30/20 breakdown of how to budget. (Remember to combine your incomes if you have a spouse or partner).

- 50% of your monthly income is spent on essentials

- 30% is spent on the fun stuff and treats

- 20% is spent on paying off debt or putting towards savings

How does inflation affect your earnings?

Inflation can reduce the purchasing power of your money because prices for goods and services go up as inflation rises. If you get a 5% rise in your wage, you might assume that gives you extra money every month to spend. But if inflation is at 10%, your wage is actually 5% behind and unable to keep up with the cost of living.

If your annual salary is £25,000:

- To keep up with the most recently published inflation rate (4.7%, October 2023), your pay would need to increase to: £26,175: a pay increase of £1,175 per year

- If your pay increased in line with current average pay growth (7.9%, September 2023), it would increase to: £26,975: a pay increase of £1,975 per year

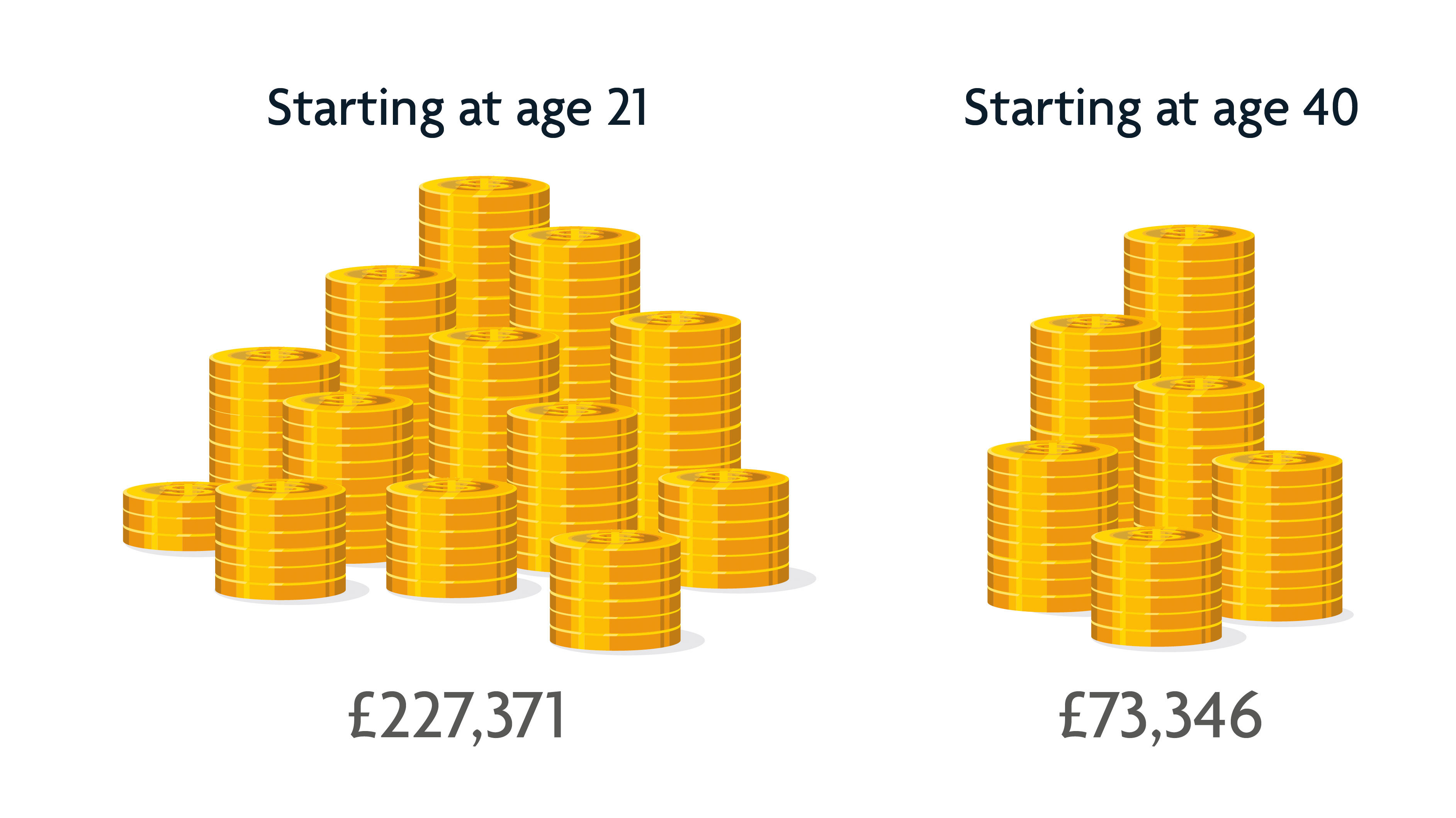

The Potential Benefits of Starting Early

*This example is based on the assumption of a 5% investment growth each year after costs and that you don’t take out a 25% tax-free lump sum at 55. If you’re 21 and start putting £200 into a pension each month, your pot may be worth £227,371 if you retire at 68.* However, if you opt out of your pension scheme and delay starting until aged 40, the fund may only be worth around £73,346.

Saving £200 into a pension each month

Starting at age 21

£227,371

Starting at age 40

£73,346

The value of investments and any income from them can fall as well as rise and you may not get back the original amount invested.

Tax concessions are not guaranteed and may change in the future. Tax free means the investor pays no tax.

Get in touch

Speak to your adviser to help you maximise your earnings and for guidance in areas like pension contributions. Please get in touch to arrange a time to chat.

Approved by The Openwork Partnership on 28.11.2023

Please note: by clicking this link you will be moving to a new website. We give no endorsement and accept no responsibility for the accuracy or content of any sites linked to from this site.